25th May, 2026| Konika Gayen| 5 Minutes Read

Forms 15G and 15H have been replaced by form 121. Learn who is affected, how TDS rules may change, and what taxpayers need to know.

If you or your family members — especially senior citizens — submitted the old forms this financial year, your bank may still deduct TDS. Here is everything you need to know about form 121.

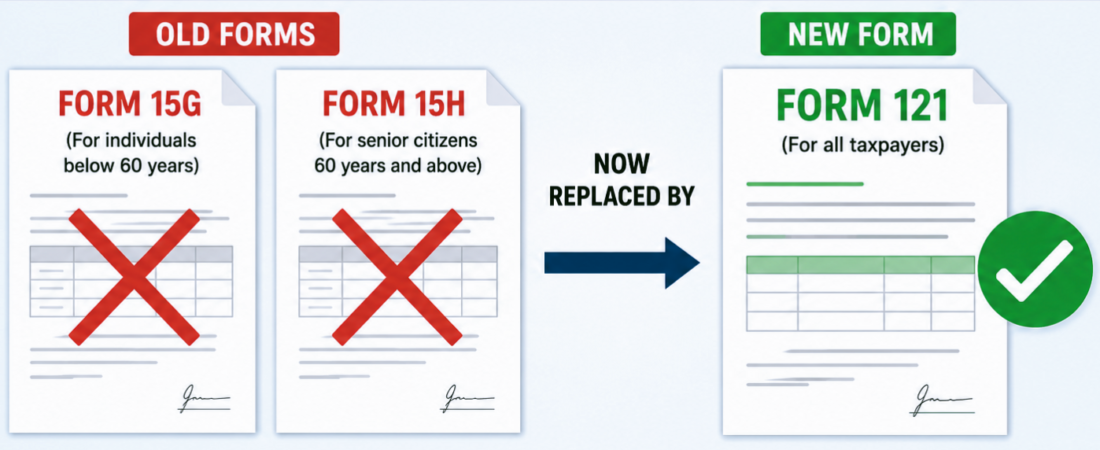

What Were Form 15G and Form 15H?

Form 15G and Form 15H were self-declaration forms that you could submit to your bank or financial institution to request that TDS (Tax Deducted at Source) not be deducted from your income — typically interest earned on fixed deposits, savings accounts, dividends, or rent.

The key condition: your total income for the year had to be below the taxable limit, meaning your tax liability was nil.

The difference between the two forms was simply age:

- Form 15G was for individuals below 60 years of age

- Form 15H was for senior citizens aged 60 and above

This age-based split often caused confusion, especially in households where people were unsure which form applied to them. That confusion ends now.

What Is Form 121?

You are eligible to submit Form 121(https://www.incometaxindia.gov.in/documents/d/guest/fn-121) if:

- You are a resident Indian (individuals and HUFs)

- Your total income is below the taxable limit — ₹2.5 lakh under the old tax regime or ₹4 lakh under the new tax regime

- Your tax liability for the year is nil

Important: NRIs (Non-Resident Indians) cannot use Form 121. This form is strictly for resident taxpayers only.

What Income Does Form 121 Cover?

You can submit Form 121 to prevent TDS deduction on:

- Interest income from Fixed Deposits (FDs)

- Interest from savings accounts

- Dividends from shares or mutual funds

- Rent income

- PF withdrawals (submitted to EPFO)

- Other specified incomes where TDS normally applies

What Is New About Form 121 Compared to 15G/15H?

Beyond merging into a single form, there are two significant changes:

1. No more age distinction The old system required you to know whether you were filing 15G or 15H based on your age. Form 121 removes this completely — one form works for everyone, whether you are 35 or 75.

2. Unique Identification Number (UIN) Every Form 121 you submit must now be assigned a 26-character Unique Identification Number by the payer (your bank, for example). This ensures your declaration is properly tracked and cannot go “missing” during tax assessments — a common problem in the past.

A Critical Misconception to Clear

Many people believe that submitting Form 15G or 15H means they do not have to pay tax at all. The same misconception applies to Form 121.

This is wrong.

Form 121 only prevents the deductor (your bank) from deducting TDS upfront. If your actual income at the end of the year turns out to be above the exemption limit, you are still required to pay tax by filing your Income Tax Return (ITR). Submitting a false declaration can lead to penalties and legal action under the Income Tax Act 2025.

Submit Form 121 only if you are genuinely eligible — that is, your total income across all sources will be below the taxable limit for that financial year.

Other Important Tax Form Changes in 2026

Form 121 is not the only change. The new Income Tax Act 2025 has renamed and restructured several key forms:

| Old Form | New Form | Purpose |

|---|---|---|

| Form 15G | Form 121 | Nil TDS declaration (below 60 years) |

| Form 15H | Form 121 | Nil TDS declaration (senior citizens) |

| Form 16A | Form 131 | TDS certificate for non-salary income |

| Form 15CA | Form 145 | Foreign remittance declaration |

| Form 15CB | Form 146 | Accountant certificate for foreign remittances |

| Form 26AS | Form 168 | Annual tax statement / tax passbook |

If you or your CA have been using these forms, make sure to update to the new numbers immediately.

What Should You Do Right Now?

Step 1: Check whether your total income for Tax Year 2026-27 will be below the taxable limit.

Step 2: If yes, do not submit Form 15G or 15H. They are no longer valid.

Step 3: Download or access Form 121 from your bank’s website or the Income Tax portal (incometax.gov.in).

Step 4: Submit Form 121 to every institution that pays you income subject to TDS — your bank, your tenant’s property manager, EPFO, etc. You must submit it separately to each payer.

Step 5: Keep a copy of your Form 121 and note the UIN allotted by each institution for your records.

The Bottom Line

The Government of India has simplified a decades-old process. Two forms are now one. The age barrier is gone. The process is being digitised.

But simplification only helps if you know about it. Millions of Indians — particularly senior citizens who diligently submitted Form 15H every April — may not be aware that the form they are used to no longer exists. If they submit the old form or fail to submit any form, their banks may deduct TDS unnecessarily.

Share this with your parents, grandparents, and anyone who earns interest income from a bank. Knowing your rights means knowing when the rules change — and acting on time.

This article is for informational purposes only and does not constitute legal or tax advice. Tax laws are subject to change. Please consult a qualified CA for advice specific to your situation.

© Know Your Rights India