A Complete Guide for Central Government Employees

Applicable to: Central Govt. Employees (Pre-2004) | Governed by: CCS (Pension) Rules, 2021 | Based on: 7th Pay Commission

By Konika Gayen, Know Your Rights India

For millions of government employees and pensioners in India, pension is one of the most important sources of financial security after retirement. But many people still get confused between Pension and Family Pension — especially regarding who receives it, how much is paid, and what happens after the pensioner’s death.

Understanding these rules is extremely important not only for retired employees but also for their families. In this article, we will explain the difference between Pension and Family Pension in the simplest way possible.

What is Pension?

A pension is a monthly payment made by the government to a retired employee as a reward for years of dedicated service. Once a government employee retires, they receive pension every month for the rest of their life.

Under the 7th Pay Commission, the pension amount is calculated as 50% of the last drawn basic pay. For example, if your last basic pay was ₹50,000, your monthly pension would be ₹25,000.

Commutation of Pension

A retiree can choose to commute up to 40% of their pension — meaning they take a one-time lump sum amount upfront. In return, the monthly pension is reduced proportionately for the next 15 years, after which the full amount is restored.

This is one of the most attractive features of the government pension scheme, particularly for its tax benefits.

What is Family Pension?

Family Pension is a monthly payment made to the surviving family members of a deceased government employee or pensioner. Instead of the pension stopping upon the employee’s death, the government continues to provide financial support — but now to the family.

An important point that many people overlook: Family pension is also payable if the employee dies while still in service, before retirement. A minimum of 7 years of government service is required for family pension eligibility.

How Much Does the Family Receive?

Family pension is paid at two different rates:

- Enhanced Rate (50% of last basic pay): Paid for the first 7 years after the employee’s death, or until the employee would have turned 67 years old — whichever comes first.

- Ordinary Rate (30% of last basic pay): Paid after the enhanced period ends, for the remainder of the recipient’s life.

Who is Eligible for Family Pension?

There is a defined priority order for who receives the family pension:

- Spouse

The husband or wife of the deceased receives family pension for life. However, it ceases upon remarriage. - Children

If there is no surviving spouse, or after the spouse’s death, eligible children receive the pension. Children remain eligible up to age 25, or until they are married or gain employment — whichever comes first. - Disabled Children

A child who is mentally or physically disabled and incapable of supporting themselves is eligible for family pension for their entire lifetime, regardless of age. This is a critical exception that ensures long-term support for vulnerable dependents. - Dependent Parents

If there is no surviving spouse and no eligible children, the dependent parents of the deceased government employee can claim family pension.

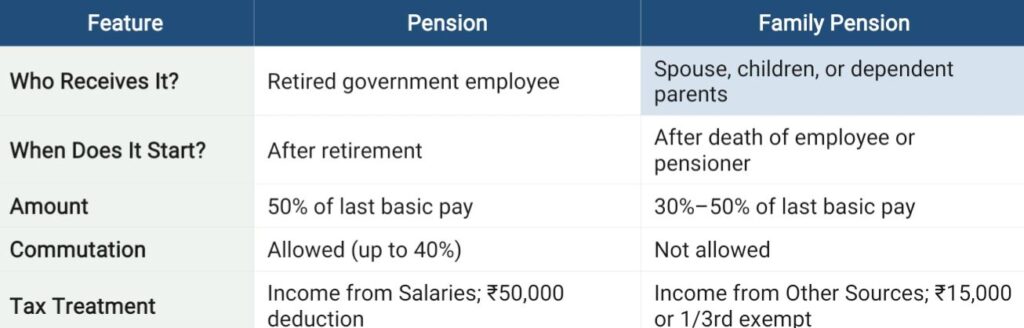

Key Differences at a glance.

Special Cases Worth Knowing

Double Family Pension

If both husband and wife were central government employees and both pass away, their children are eligible to receive two separate family pensions — one from each parent’s service record.

Dearness Relief (DR)

Family pension is not a fixed amount forever. Just like regular pension, it is revised periodically through Dearness Relief increases to account for inflation, ensuring the purchasing power of the recipient is maintained.

Divorced or Widowed Daughters

A divorced or widowed daughter who is not employed can also be eligible for family pension under certain conditions — even if she is above 25 years of age.

Governing Rules

All the provisions discussed in this article are governed by the Central Civil Services (Pension) Rules, 2021 for central government employees. State government employees are subject to their respective state pension rules, which may differ in details.

Tax Rules Explained

The tax treatment of pension and family pension is significantly different, and understanding these rules can help in better financial planning.

1. Regular Pension — Taxed as Salary

Monthly pension received by the retired employee is taxed under the head ‘Income from Salaries’. It is added to the total income and taxed as per the applicable income tax slab.

However, retirees can claim a standard deduction of ₹50,000 — just like regular salaried employees. This effectively makes the first ₹50,000 of annual pension tax-free.

Note: Dearness Relief (DR) received along with pension is also fully taxable.

Example: Annual pension of ₹3,00,000 minus ₹50,000 standard deduction = ₹2,50,000 taxable income.

2. Family Pension — Taxed as Other Income

Family pension is taxed under ‘Income from Other Sources’ — not salary. This means the standard deduction does not apply. Instead, a special exemption is available:

Exemption = Lower of: ₹15,000 OR 1/3rd of total family pension received in the year

The table below illustrates how this works at different pension levels:

3.Commuted Pension — 100% Tax-Free

This is one of the most significant tax advantages available to government employees. When a retiree commutes part of their pension (takes a lump sum at retirement), the entire lump sum is completely tax-free under Section 10(10A) of the Income Tax Act.

For example, if you commute 40% of your pension and receive ₹10 lakhs as a one-time payment — you pay zero tax on that amount. For private sector employees, only a partial exemption is available.

Summary of tax rules:

Pension is the financial security you earn for yourself after years of government service. Family Pension is the safety net your loved ones receive after you are gone. Both are equally important, and understanding the rules — especially around eligibility, rates, and taxes — can make a significant difference to your family’s financial future.

If you are a government employee who joined before January 1, 2004, you are covered under the Old Pension Scheme (OPS) and are entitled to these benefits. Always ensure that your service records are updated and that your family is aware of their entitlements.

Disclaimer: This article is for informational purposes only. All figures are based on the 7th Pay Commission and CCS (Pension) Rules, 2021. For personalized advice, consult your department’s pension cell or a qualified financial advice.