A Comprehensive Guide to the National Pension System

Updated: May 2026 | Regulated by PFRDA, Government of India

By Konika Gayen, Know Your Rights India (10 minutes read)

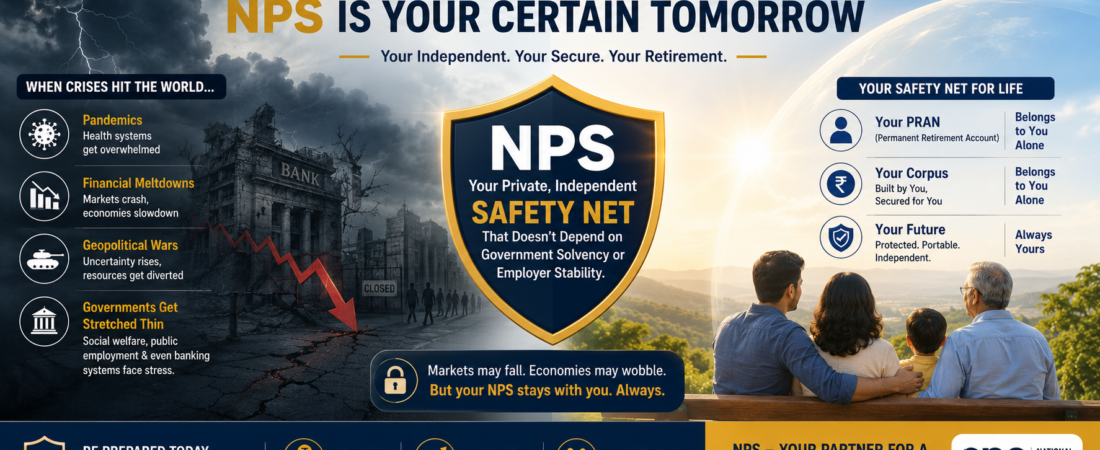

During global crises — pandemics, financial meltdowns, geopolitical wars — governments get stretched thin. Social welfare, public employment, and even banking systems face stress.NPS acts as your private, independent safety net that doesn’t depend on government solvency or employer stability. Your PRAN (Permanent Retirement Account) and corpus belong to you alone.The biggest mistake investors make during crises is stopping contributions. NPS’s lock-in structure actually protects you from this — your money stays invested and keeps compounding even through downturns. Historically, markets recovered, and those who stayed invested came out ahead.

The biggest mistake investors make during crises is stopping contributions. NPS’s lock-in structure actually protects you from this — your money stays invested and keeps compounding even through downturns. Historically, markets recovered, and those who stayed invested came out ahead.

In a landmark development on May 17, 2026, PFRDA introduced the Retirement Income Scheme (RIS) — a transformative framework that gives NPS subscribers the power to withdraw their entire corpus in a phased, structured manner up to the age of 85. This upgrade fundamentally changes how Indians can access and manage their retirement wealth, offering unprecedented flexibility during the decumulation phase of life.

What Is the National Pension System?

Planning for retirement is one of the most important financial decisions you will ever make. In a country like India, where social security systems are still developing, building your own retirement corpus is not just wise — it is essential. The National Pension System (NPS) is one of the most powerful and tax-efficient tools available to every Indian citizen today.

Introduced by the Government of India in 2004 and regulated by the Pension Fund Regulatory and Development Authority (PFRDA), NPS has evolved from a mandatory scheme for government employees into a flexible, market-linked retirement solution open to all. With over 9 crore subscribers and assets under management (AUM) crossing Rs. 16 lakh crore in 2025, NPS has become the backbone of retirement planning in India.

The National Pension System is a defined contribution, market-linked, voluntary retirement savings scheme. Unlike traditional pension plans that offer a fixed guaranteed payout, NPS invests your contributions across a mix of equities, corporate bonds, and government securities — generating returns linked to market performance.

NPS is open to all Indian citizens between the ages of 18 and 85 years, including Non-Resident Indians (NRIs). It is mandatory for all Central Government employees who joined service on or after January 1, 2004. For all others, it is a powerful voluntary option.

Key Features at a Glance

- Simple and transparent — 24/7 online account access with regular disclosures

- Portable — account follows you across jobs and cities with a single PRAN (Permanent Retirement Account Number)

- Flexible — choose your investment strategy, asset allocation, and fund manager

- Low cost — one of the most cost-effective long-term retirement products in India

- Tax efficient — multiple layers of tax deduction available under the Income Tax Act

- Regulated — governed by PFRDA with strong investor protection norms

Understanding NPS Account Types

Tier I — The Core Retirement Account

Tier I is the primary NPS account and the foundation of your retirement planning. Contributions here are locked in until you reach the age of 60, except under specific circumstances such as higher education, critical illness, or purchase of a first home. This enforced discipline ensures your retirement corpus remains intact and grows over the long term.

Tier I accounts enjoy the most comprehensive tax benefits under Sections 80C and 80CCD(1B) of the Income Tax Act. The minimum contribution to keep the account active is just Rs. 500 per month, making it accessible to virtually all income groups.

Tier II — The Flexible Savings Account

Tier II is an optional add-on account available only to those who already have a Tier I account. Unlike Tier I, Tier II has no lock-in period — you can withdraw funds anytime. This makes it function more like a savings or liquid investment account.

However, Tier II does not offer the same tax benefits as Tier I for most investors (except central government employees, for whom Tier II has a 3-year lock-in with tax deduction).

Investment Options — How Your Money Grows

Other alternative instruments for portfolio diversification

- Asset Class E (Equity): Invests in stocks and equity markets. Offers the highest growth potential with higher short-term volatility. Historically delivered 14-16% per annum over long periods.

- Asset Class C (Corporate Bonds): Invests in high-quality corporate debt instruments. Balances growth and stability, typically returning 6-7% per annum.

- Asset Class G (Government Securities): Invests in central and state government bonds. The safest option, yielding 5-6% per annum with capital preservation.

- Asset Class A (Alternatives): Invests in REITs, InvITs, and other alternative instruments for portfolio diversification.

Active Choice vs. Auto Choice

- Active Choice: You decide exactly how to allocate your contributions across the four asset classes. As of October 2025, private and self-employed subscribers can now allocate up to 100% in equities under the new Multiple Scheme Framework (MSF), up from the previous cap of 75%. This is ideal for investors who are financially literate and can tolerate market volatility.

- Auto Choice: A lifecycle-based approach where allocation automatically shifts from equity to debt as you age. You can choose from three risk profiles — Conservative, Moderate, or Aggressive. This is the recommended approach for investors who prefer a hands-off strategy.

Tax Benefits — A Triple Advantage

- Section 80C: Contributions up to Rs. 1.5 lakh per year are eligible for deduction under Section 80C, along with other instruments like PPF, ELSS, and life insurance.

- Section 80CCD(1B): An additional deduction of up to Rs. 50,000 per year is exclusively available for NPS contributions. This is over and above the Rs. 1.5 lakh limit under 80C — allowing a total deduction of up to Rs. 2 lakh per year.

- Section 80CCD(2): If your employer contributes to your NPS (up to 10% of basic salary for private employees, 14% for government employees), that contribution is also tax-deductible — with no upper monetary limit.

- Tax-free on Maturity: At retirement, 60% of the corpus withdrawn as a lump sum is completely tax-free. The remaining 40% (used to purchase an annuity) generates a regular pension income.

NEW (May 2026): Retirement Income Scheme (RIS) — Withdraw Your Full Corpus by 85

What Is the RIS and Why Does It Matter?

The Retirement Income Scheme is designed to provide NPS subscribers with flexible periodic payout options during their decumulation phase (the period after retirement when you draw down your savings). The key distinction is that RIS operates on the lumpsum portion of your corpus — the amount you are entitled to withdraw at retirement — and does not affect the mandatory annuity requirement.

In simpler terms: even while receiving monthly/quarterly payouts under RIS, your minimum 20% or 40% annuity obligation remains fulfilled separately. The RIS payouts come from your discretionary, withdrawable corpus.

RIS Eligibility

- All government NPS subscribers.

- All non-government NPS subscribers (NGS).

- Subscribers who wish to receive systematic payouts from their designated pension corpus.

- Eligible up to a maximum age of 85 years.

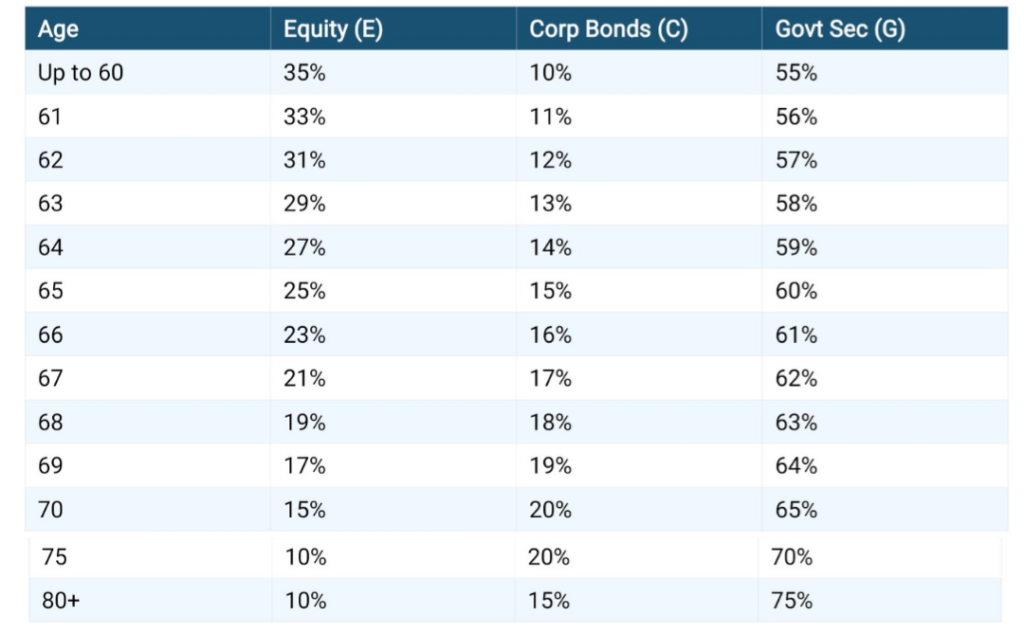

RIS Steady — The Age-Based Glide Path Investment Strategy

Under RIS Steady, PFRDA has designed a continuously declining equity glide path. As a retiree ages, their investment automatically shifts from equity-heavy to government securities-heavy, providing growth in early retirement and capital protection in later years.

Payout Frequency Options

Under RIS, subscribers can choose to receive their phased payouts on any of the following frequencies:

Monthly

Quarterly

Half-yearly

Annually

The choice of payout frequency is made at the time of closure of the pension account (exit from NPS), after which fresh contributions stop. Once selected, the payout method applies throughout the drawdown period.

What Happens If the Subscriber Passes Away During Drawdown?

If a subscriber using the RIS drawdown facility passes away during the payout phase, the remaining balance in their NPS account — after accounting for any payments already made — is paid in full to the subscriber’s nominee or legal heir as per existing PFRDA regulations. The corpus is never forfeited.

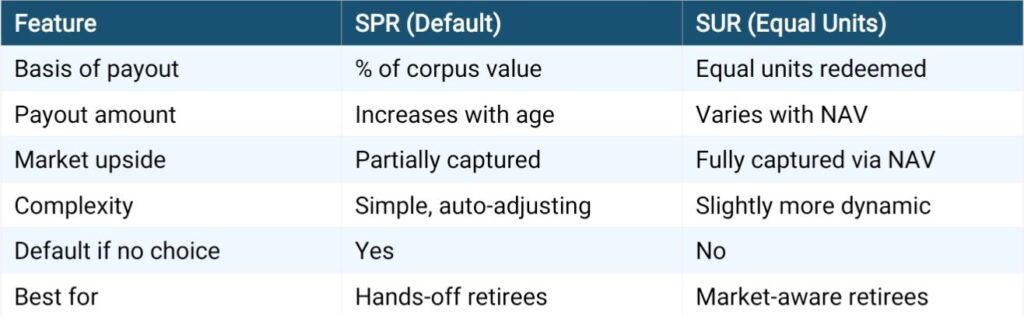

NEW (May 2026): NPS Drawdown Options — SPR and SUR Explained

PFRDA has introduced two drawdown methods under the RIS framework. Subscribers choose one at the time of NPS exit. If no choice is made, the Systematic Payout Rate (SPR) is applied by default.

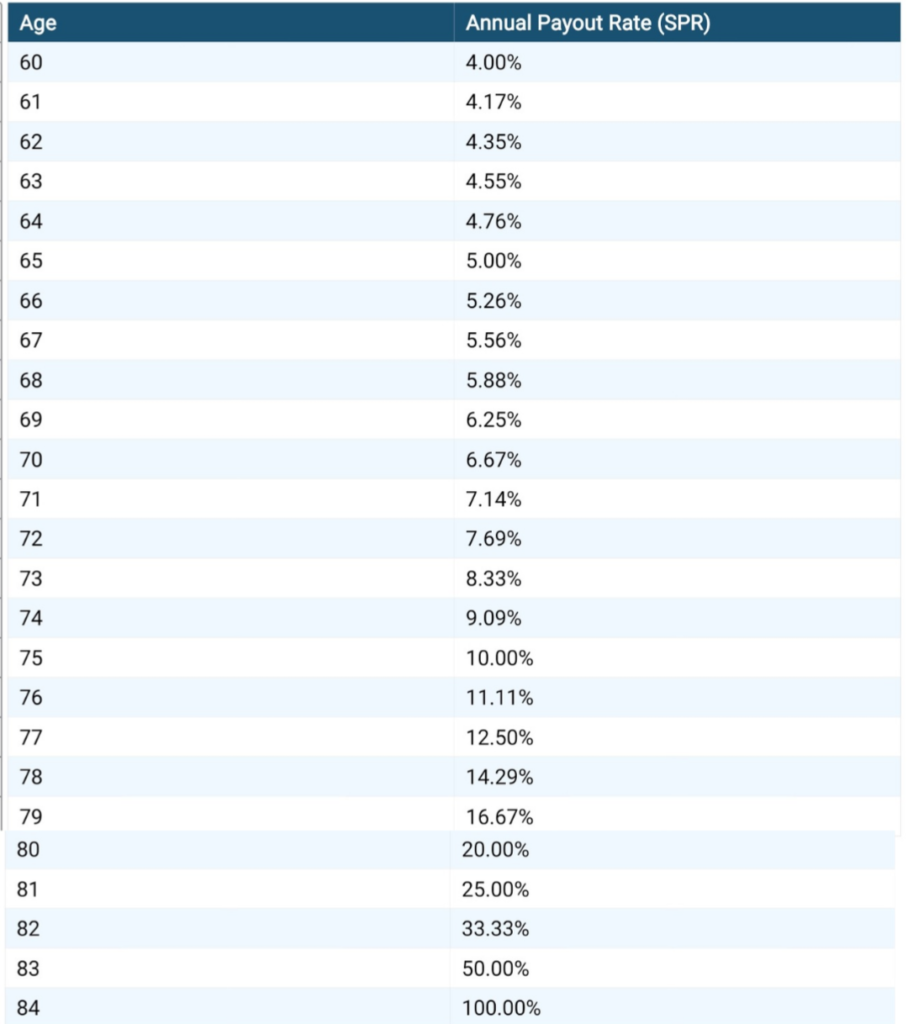

Option 1: Systematic Payout Rate (SPR) — Default

The SPR is a formula-driven method where the annual payout is calculated as a percentage of the remaining corpus, based on the subscriber’s current age and the fixed drawdown end age of 85.

SPR Formula: SPR = 1 ÷ (Drawdown End Age − Current Age)

This means the payout rate increases every year as the subscriber grows older, ensuring that the corpus is fully drawn down by age 85.

Examples:

At age 60: 1 ÷ (85 − 60) = 4.00% of corpus withdrawn annually

At age 65: 1 ÷ (85 − 65) = 5.00% of corpus withdrawn annually

At age 70: 1 ÷ (85 − 70) = 6.67% of corpus withdrawn annually

At age 75: 1 ÷ (85 − 75) = 10.00% of corpus withdrawn annually

At age 84: 1 ÷ (85 − 84) = 100.00% — entire remaining corpus withdrawn

The SPR resets automatically every year on the subscriber’s birthday, based on the prevailing market value of the corpus at that time. This means payout amounts adjust dynamically with market performance — if the corpus grows, payouts grow too.

Complete SPR Payout Rate Table (Age 60 to 84):

The SPR method is ideal for subscribers who want automatic, self-adjusting payouts without manual intervention — the system handles everything.

Option 2: Systematic Unit Redemption (SUR) — Equal Units

Under SUR, the total number of NPS units held at the start of the drawdown are divided into equal instalments, which are redeemed at each payout frequency over the selected drawdown period (up to age 85).

SUR Formula: Units per period = Total Units ÷ Drawdown Period × Payout Frequency

Practical Example:

Corpus at exit: Rs. 80 lakh

NAV at drawdown start: Rs. 10.00 per unit

Total units: 8,00,000 units

Age at exit: 60 years | Drawdown period: 25 years (up to 85)

Payout frequency: Monthly (12 per year)

Units per month: 8,00,000 ÷ 25 × 12 = 2,666.67 units per month

Monthly payout value varies with NAV — if NAV rises, payout value rises

The SUR method is suitable for subscribers who prefer equal-unit redemption and want their payout amounts to benefit from potential NAV appreciation over time. It provides a degree of upside participation in market growth even during the retirement drawdown phase.

SPR vs. SUR — Which Should You Choose?

Major 2025 Reforms — NPS Gets a Big Upgrade

The year 2025 brought transformative changes to NPS, making it more flexible and aligned with modern investor needs. Here are the most significant updates:

Multiple Scheme Framework (MSF)

The new Multiple Scheme Framework allows non-government subscribers to hold and invest in multiple NPS schemes simultaneously under a single PRAN. This enables better diversification across different fund managers, risk profiles, and investment strategies — all under one account. Each MSF scheme comes with a risk-o-meter to help investors assess risk before investing.

100% Equity Allocation Now Allowed

From October 1, 2025, private, corporate, and self-employed subscribers can allocate up to 100% of their NPS contributions to equities under eligible MSF schemes. Previously, equity allocation was capped at 75%. This is a landmark change that allows younger, risk-tolerant investors to maximize long-term growth potential through equity.

Reduced Mandatory Annuity Requirement

The mandatory annuity purchase at retirement has been reduced from 40% to just 20% of the total corpus for non-government subscribers (subject to conditions). This means up to 80% of your accumulated wealth can now be withdrawn as a lump sum or through systematic withdrawal, giving you far greater control over your retirement income.

NPS Vatsalya — Start Early for Your Children

The NPS Vatsalya scheme allows parents to open an NPS account in the name of their minor children. Contributions can be made monthly or annually until the child turns 18. At that point, the account seamlessly converts to a standard NPS account. Budget 2025 extended full NPS tax benefits to NPS Vatsalya accounts — making it an excellent vehicle to begin retirement planning from childhood.

Strategies to Maximize Your NPS Returns

- At Retirement (Age 60): You can withdraw up to 80% of your corpus as a lump sum (of which 60% is tax-free). The remaining minimum 20% must be used to purchase an annuity plan that provides a regular monthly pension.

- Early Exit (Before Age 60): If you exit before 60 after completing at least 5 years, you must use at least 80% of the corpus to buy an annuity and can withdraw 20% as a lump sum. However, if the total corpus is below Rs. 5 lakh, 100% can be withdrawn.

- Partial Withdrawal: After 3 years in NPS, you can partially withdraw up to 25% of your own contributions for specific purposes such as higher education, marriage, critical illness, or purchase of a first home.

- On Death: The entire corpus (100%) is paid to the subscriber’s nominee or legal heir — no mandatory annuity purchase required.

Who Should Invest in NPS?

NPS is ideally suited for a wide range of investors:

- Salaried professionals in the private sector looking to supplement EPF/EPFO savings with market-linked growth.

- Self-employed individuals and freelancers who have no employer-sponsored pension plan.

- Government employees who are already enrolled and wish to optimize their contributions.

- Young investors (18–35) who want to build a large corpus by starting early with equity-heavy allocations.

- Conservative investors who prefer a regulated, low-cost alternative to direct equity or mutual funds.

- Parents who want to start retirement planning for their children via NPS Vatsalya.

Your future self will thank you for the decision you made today.

The National Pension System is no longer just a government employee’s mandatory scheme. It has evolved into one of India’s most sophisticated, flexible, and tax-efficient retirement planning tools — now enhanced significantly by the 2025 PFRDA reforms.

The key to unlocking the full potential of NPS is simple: start early, stay consistent, choose the right asset allocation for your age and risk appetite, and review your portfolio annually. Whether you contribute Rs. 500 or Rs. 50,000 a month, every rupee invested in NPS today is a step toward a dignified, financially independent retirement.