India’s central bank built a record dollar short book trying to save the rupee. Now that position may be making things worse.

Published: May 2026| Konika Gayen| 5 minutes read

THE SCALE OF THE FALL

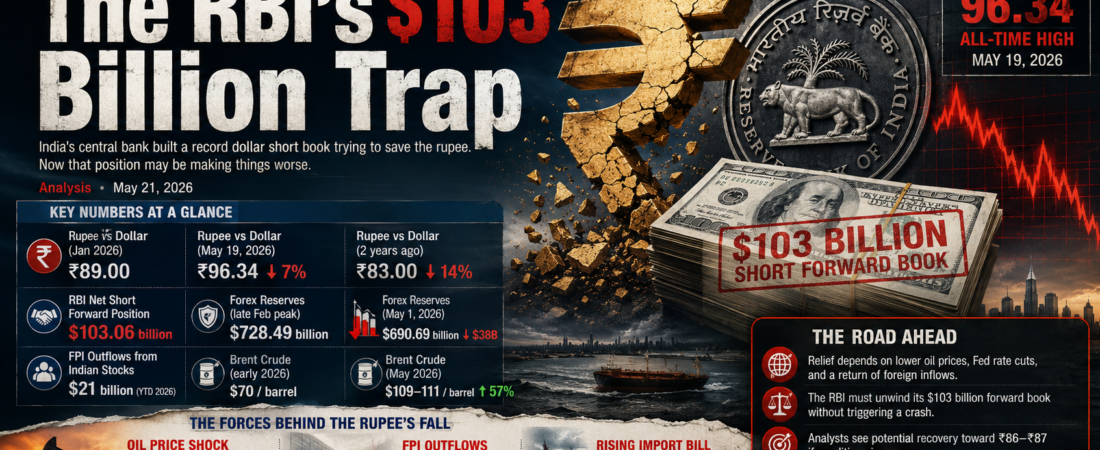

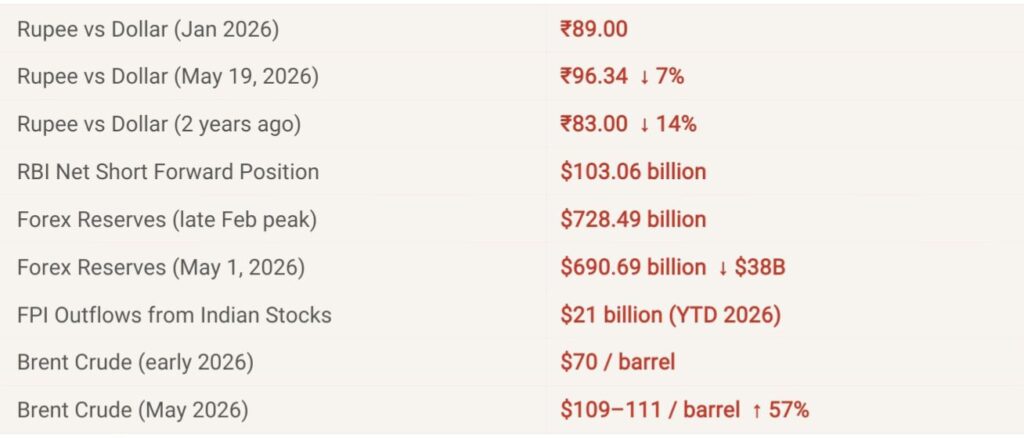

The rupee breached ₹90 in late February. It crossed ₹95 for the first time in late March. By mid-May it had set fresh all-time lows in five of seven consecutive trading sessions. From ₹83 two years ago to ₹96 today, India’s currency has lost roughly 14% of its value against the dollar — one of the steepest sustained declines since the taper tantrum of 2013.

For most people, this registers as an abstraction. But a weaker rupee means more expensive fuel, higher imported inflation, costlier foreign education and travel, and a heavier burden on any Indian business that pays its bills in dollars. It also signals something deeper: that India’s external position — the balance of what it earns and what it owes internationally — is under serious stress.

“The rupee has set fresh all-time lows in five of the last seven trading sessions.”

HOW A CENTRAL BANK DEFENDS ITS CURRENCY

When a currency falls too fast, a central bank has two primary tools:

- The first is direct: sell dollars from its foreign exchange reserves into the market, increasing dollar supply, supporting the local currency. India’s reserves, which peaked at $728 billion in late February, have fallen to $690 billion by May — a drain of nearly $38 billion in roughly two months. That is the visible cost of defence.

- The second tool is less visible and more complex: the forward market. Instead of selling dollars today, the central bank can commit to selling dollars in the future at pre-agreed prices. These are called short dollar forward positions. The advantage is that it allows the RBI to support the rupee without immediately depleting its published reserve figures. It is, in effect, borrowing from the future to defend the present.Used carefully, this is a legitimate and widely-used tool. Used at scale, under sustained pressure, it becomes a trap.

THE $103 BILLION COMMITMENT

By the end of March 2026, the Reserve Bank of India’s net short dollar position in the forward market had reached $103.06 billion — a 34% jump from $77.25 billion just one month earlier in February. Short-term positions surged from $28 billion to $51 billion in that single month. Positions of greater than one year stood at $52.8 billion.

To understand why this matters, consider what these numbers represent. Each dollar in the forward book is a legally binding promise the RBI has made to deliver dollars to banks and market participants at a future date. As those contracts mature — week by week, month by month — dollars flow out of the system. That outflow adds selling pressure on the rupee at the exact moment the RBI is trying to prevent selling pressure on the rupee.

“Until the RBI unwinds its forward positions, fresh foreign inflows are unlikely to return.”

The market understands this dynamic. Foreign institutional investors, who might otherwise bring capital back into Indian equities and debt, are holding back. The reason is simple: they know that the pipeline of dollar outflows from the RBI’s maturing forward contracts will continue to weigh on the rupee. Investing in rupee assets while that pipeline is open means absorbing currency losses before any returns. As one senior forex analyst noted, until the RBI unwinds its forward positions, fresh foreign inflows are unlikely to return.

The trap is structural. The RBI cannot easily unwind — doing so quickly would itself require buying dollars and putting pressure on its reserves. And it cannot stop the contracts from maturing. So for months to come, every forward contract that falls due will release more dollar demand into the market, and the rupee will feel it.

THE OIL STORM BEHIND THE CRISIS

The RBI did not create this situation in isolation. It was responding, month after month, to an external shock of remarkable scale: a 57% surge in crude oil prices driven by escalating Middle East conflict.

Brent crude went from below $70 per barrel in early 2026 to above $109 in May. India imports 85 to 88% of its crude oil and pays for it in US dollars. Every dollar rise in the oil price adds approximately ₹17,000 crore to India’s annual import bill. At $111 versus $70, the annualised increase in India’s crude import cost is roughly $60 billion — a current account shock of historic proportions.

India’s state-owned oil marketing companies — the OMCs — became relentless buyers of dollars in the foreign exchange market. That structural, daily demand for dollars to pay for oil became the dominant mechanical driver of rupee weakness. The RBI stepped in with forward contracts to slow the fall. But the oil price did not fall. And so the forward book grew, and grew, and grew.

At the same time, foreign portfolio investors withdrew roughly $21 billion from Indian equities in 2026 alone. When investors exit Indian stocks, they convert rupees into dollars to repatriate the money. That added another layer of dollar demand — arriving precisely when oil importers were already overwhelming the market.

THE RESERVE DRAIN

India’s foreign exchange reserves — the real, usable stockpile — tell a parallel story of stress. The reserves peaked at $728.49 billion in late February. By the week ending May 1, they had fallen to $690.69 billion. In a single week that month, they dropped $7.79 billion: $2.8 billion in foreign currency assets and $5 billion in gold reserves.

On paper, $690 billion is a substantial buffer — enough to cover more than 11 months of imports, which is strong by international standards. But there is a catch. Those headline figures do not account for the $103 billion in forward book obligations sitting off the balance sheet. When analysts adjust the import cover for the forward book, the effective buffer looks considerably thinner. The aggressive pace of drawdown has revived memories of previous Indian currency crises and drawn unflattering comparisons to the far larger reserve cushions maintained by economies like China.

THE PATH FORWARD

The near-term pressure on the rupee is real and the tools available to arrest it are constrained. The RBI has already introduced additional measures — including a cap of $100 million on banks’ daily net open rupee positions, a dramatic reduction from the previous 25% of total capital limit — in an effort to curtail speculative selling. But these are defensive moves.

The recovery case hinges on external factors largely outside India’s control:

a fall in oil prices if Middle East tensions ease, a Fed rate cut that weakens the dollar globally, a reversal of foreign outflows as India’s relative growth story reasserts itself. In that scenario, analysts at institutions including Bank of America and ING project the rupee recovering toward ₹86 to ₹87.

But even in a recovery, the RBI will eventually need to unwind its $103 billion forward book. That unwinding will itself generate dollar outflows and create headwinds for the rupee. There is no clean exit. The position that was built to defend the currency must now be carefully dismantled without triggering the very crash it was designed to prevent.

The historical parallel that analysts keep returning to is 2013. During that taper tantrum, India faced a sharp rupee slide and stabilised it through a combination of tools — tighter liquidity, import restrictions, and credible central bank communication. But 2013 was a capital flow shock. This is an oil price shock, a geopolitical shock, a capital outflow shock, and a central bank balance sheet problem — all at the same time.

“There is no clean exit. The position built to defend the currency must now be dismantled without triggering the crash it was designed to prevent.”

The Indian rupee’s fall is a story about compounding vulnerabilities. A commodity shock that India cannot hedge. A central bank that overextended its tools in a well-intentioned effort to buy time. A global investor community that is watching and waiting for a signal that the worst is over.

The ₹100 level — unimaginable two years ago — is no longer dismissed as fantasy. No mainstream institution projects it in 2026. But it is no longer absurd to model the scenario in which it arrives. That alone is a measure of how much ground has been lost.

For ordinary Indians, the fall matters in ways that never make the financial headlines: the cost of cooking gas, the price of imported electronics, the affordability of a foreign university. For policymakers, it marks the limits of what a central bank can do alone when the forces arrayed against it are this large.

The RBI’s $103 billion forward book is not a footnote. It is the heart of this story.

Data sourced from RBI monthly bulletins, Bloomberg, Bank of America, ING Research, and CR Forex. Figures current as of May 19–21, 2026.